Potential Investors,

One of the most asked questions we get from our prospective investors is to explain how they are getting paid when they invest with us and how they can measure their investment’s performance. We use three main metrics to measure our property’s performance for our Investors. In this article we will discuss the three main metrics we use to evaluate our investment returns, pros and cons of the three, what you should be looking for when you invest, and how Criterion structures our returns.

Cash-on-Cash (“CoC”)

Formula - [Distributions Received per Year / total Funds Remaining in investment** = Annual Cash on Cash %]

Cash-on-Cash is by far the easiest investment return metric to understand. Simply stated, CoC is the cash you receive in distributions per year as the numerator* with the total cash you have remaining in the investment acting as the denominator**. For example, if you invested $100,000 and received $12,000 in distributions in that calendar year, you received a 12% CoC return on your investment for that year.

CoC is an important metric when evaluating real estate investments because it generally assumes that the property is, or is planning to be, cash flowing (see One of the Top Five Reasons to Invest in Commercial Real Estate here) Investors like CoC because you do not have to wait years and years for the appreciation and sale of the property to see if your investment is performing well. At Criterion, we strive to pay out double digit COC (10%+ Annually) paid out quarterly. This allows our Investors to know immediately how well the property is performing.

*The numerator should only include distributions that are considered Return on Capital, or “profit”, and not Return of Capital, or the return of your investment.

**The denominator of the formula should be the total funds remaining in the investment. Using the same example above; if you invested $100,000, the property was refinanced, and you received a return via Return of Capital of half of your investment, your remaining cash in the investment would be $50,000 and the $12,000 in distributions would equate to a 24% CoC return since you only have $50,000 remaining in the investment.

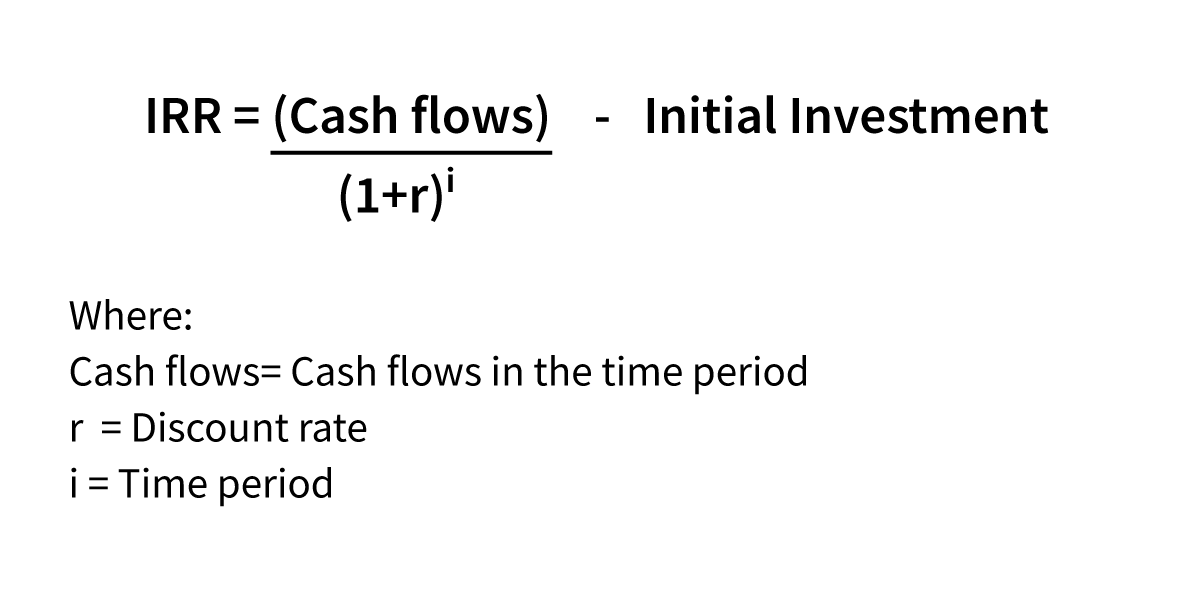

Internal Rate of return (“IRR”)

formula

To define IRR might make you more confused, but I would still like for you to have the definition and then I can break it down from there.

Internal Rate of Return -

“a discount rate that makes the net present value (NPV) of all cash flows from a particular project equal to zero.” - Investopedia (https://www.investopedia.com/terms/i/irr.asp)

IRR starts to get a bit more complex when it comes to understanding investment metrics, but the main difference when comparing CoC vs IRR is that CoC doesn’t include the time value of money. IRR requires assumptions such as sales price and the duration of the investment (with any sort of modeling, the outputs are only as good as the assumptions you input).

The total cash flows, or numerator, should be inclusive of the initial investment, all cash flows produced while the asset is held, and the total cash distributed at the sale including your original investment (this would include the debt pay down, any appreciation in the property, and the original equity returned).

Example: You had an initial investment of $1,015,000 into a development and it wasn’t expected to produce any cash flow until you sold the building 18 months later.

In this example you can see that the first year is negative because of the initial investment. It is important to note that the $1,467,862.72 received in month 18 also includes the original investment of $1,015,000 thus making the total profit $452,862.72. You can also see from the time the investment was made until the time the final distributions were made 18 months later your IRR is 24.85%.

In the simplest form possible, IRR is the forecasted rate of growth by isolating the effect of compounding interest if the investment term is over one year.

Although the IRR metric is widely used it has a lot of shortcomings. It requires some major assumptions on the assumed sale price of the property along with an assumed sale date. It also assumes that the cash flows are reinvested at some rate. You can now start to see the value of positive cash flow and the CoC metric. CoC requires no patience or modeling because its distributed cash from cash flow produced by the property.

Annual Return Generated

Formula - [(Annual Cash flow + Annual Debt Reduction) / Investment]

The Annual Return Generated is valuable because it not only takes into account your annual Cash-on-Cash, but also includes a reduction in debt for the year. If you had a $500,000 investment in a property that produced $100,000/year in cash flow and an additional $75,000 in principle/debt reduction then the total Annual Return Generated would be 35% as opposed to your annual CoC percentage of 20%. You can see how factoring in the annual debt reduction adds important value.

recap

Now that we have gone over the three major investment metrics that Criterion uses when offering investment opportunities we can give a brief overview of how we structure our returns based off investor feedback.

Investors like Cash. Cash Flow is King.

I know this seems like a given but it still needs to be said. Investments that start producing immediate cash flow are typically going to be received well. At Criterion we typically offer double digit CoC returns. Our investors love it and they don’t have to wait years before they see any cash flow from their investment.

IRR is nice, but don’t invest solely on the highest IRR.

IRR is nice, don’t get me wrong. It brings a lot of insight into the growth of the investment at a fixed cost of capital, but it desperately needs to be complimented with other return metrics to help support it, such as CoC and Annual Return Generated.

Compound the Growth.

Commercial Real Estate has proven to be an attractive investment due to many financial advantages. Commercial Real Estate truly “throws” cash at you from all directions. You not only get cash flow, but also you are paying down the debt and the property is appreciating through rent increases and general inflation.

Where are you investing your money, in what forms does it pay you, and how often does it pay you? Are you getting paid in cash flow or are you getting sold the promise of future performance while you wait on your returns?

These are the questions I would be asking.

Best,

Braden Cheek

Co-Founder | Criterion